Tax Implications of Selling Real Es

When the time comes to list a piece of property on the market, your clients may need to consider the potential tax liability that a sizable sale may incur. This is especially important for those who wish to use profits as income for retirement or to meet other long-term financial goals.

Understanding what future tax liability may be — particularly capital gains tax — can help you advise clients toward the best course of action, and, you may find that a traditional lump sum payment on their real estate sale may not be the most tax efficient sale structure for them. In these cases, you might consider recommending a structured installment sale (SIS).

Read a real estate case example of a structured installment sale

Below we’ll look at what types of properties are eligible, some potential tax implications, and how a structured installment sale may help defer and/or reduce your clients’ tax obligations.

Capital Gains Taxes When Selling Real Estate, Property, or Agricultural Land

In general, sellers can anticipate that the capital gains tax rate from a real estate transaction will range between 0% and 20% of the net proceeds made when selling the property. Additionally, a Net Investment Income Tax (NIIT) may apply if income exceeds certain levels. NIIT can add 3.8% in tax on top of capital gains tax.

If the seller receives the real estate sale proceeds in a lump sum, they might face not only capital gains tax, but also substantial NIIT and state income taxes, which are typically due in the year of the sale.*

*Source: IRS Topic no. 409, Capital gains and losses

How Is Capital Gains Tax Calculated?

Capital gains on the sale of real estate (such as a rental property, personal home, agricultural land, etc.) are calculated by deducting the amount paid for the property (including the cost of capital improvements) from the sale price, and subtracting any transaction costs.

A seller may be able to exclude the first $250,000 of capital gain from the sale of a primary residence ($500,000 for a married couple filing jointly) for income tax purposes, if certain conditions are met.*

*Source: IRS Topic no. 701, Sale of your home

How can a Structured Installment Sale be Used When Selling Real Estate?

A structured installment sale can be used to sell a variety of property types. An SIS allows the seller to be paid in future installments over a period of time, rather than a one-time lump sum. Because taxes would then be paid based on the income received each year, this structure allows the seller to defer their capital gains tax and potentially decrease the overall tax liability on the sale. This results in a tax-smart stream of guaranteed income.

For a transaction to qualify as a structured installment sale, it must involve the sale of an eligible property in which you receive at least one payment after the tax year of the transaction. Property types can include (but aren’t limited to):

- Personal property (such as your home)

- Commercial real estate

- Rental property

- Vacation home

- Agricultural land

- Farmland

Examples of a Real Estate Structured Installment Sale

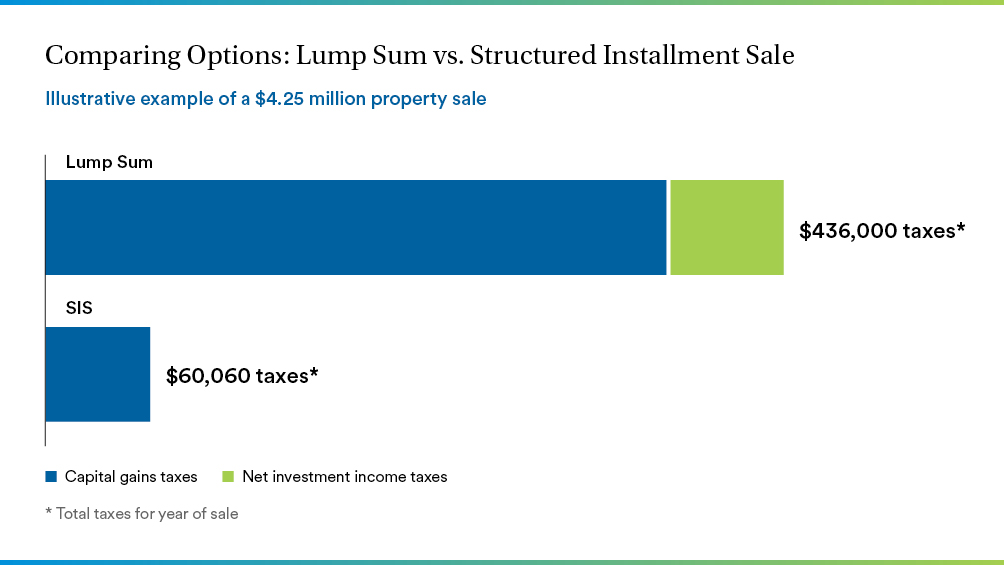

Let’s look at an illustrative example: Mary is 48 years old and has decided to sell her childhood home. After putting it on the market, she receives an offer for $4,250,000. After the property’s adjusted basis and selling expenses, Mary’s gain from the transaction will be $2,150,000, and the property is not subject to a mortgage.

Mary’s legal, tax, and financial advisors determined during the sales process that a structured installment sale would be beneficial in reducing capital gains tax and NIIT, while also providing periodic payments to supplement her retirement income. In addition, Mary’s tax advisor mentioned that taxes attributable to the sale would be reduced due to $100,000 of realized long-term capital losses within her investment portfolio.

In the property’s final purchase and sale agreement, it was determined that the home’s purchase price would be paid out in the following manner: Mary would receive a lump sum payment of $600,000 this year, and the remaining $3,650,000 would be paid in 15 equal amounts annually, beginning next year.

Benefits of a Structured Installment in a Real Estate Sale

Choosing a structured installment for a real estate transaction can have several benefits. Primarily, it has the potential to help sellers reduce their tax bills, while generating guaranteed income for retirement or other financial needs in the form of a fixed annuity.

Using the example above, let’s examine the tax savings Mary experienced by opting for a structured installment sale instead of a lump sum payment.

If Mary had received the proceeds in full at the time of the sale, she would have had to pay close to $370,582 in capital gain taxes (at a marginal 20% federal capital gains rate) and another $68,400 due to the 3.8% NIIT, for a total tax liability of around $438,900. Because Mary lives in a state with no income tax, she did not need to include that in her total tax bill.

By choosing a Structured Installment Sale, she will pay approximately $12,988.50 in taxes this year (taking advantage of the 0% and 15% capital gains tax rates) and about $22,450 in taxes annually for the following 15 years. By spreading the gain over a period of years, she will avoid net investment income taxes altogether. This results in a tax savings of over $89,000.*1

*Rates are subject to change

Offering a Structured Installment as a Buyer

For those looking to make their offer for a real estate property more attractive, a structured installment sale should be considered. Since this sale structure creates an opportunity to defer capital gains tax and offers sellers the potential to reduce their overall tax liability, it can be an effective strategy for making an offer stand out.

When it comes to transitioning assets into income for retirement, sellers may be eager to optimize their take-home profit — and a structured installment sale helps accomplish this goal.

Read a real estate case example of a structured installment sale

Finding the Right Insurer for Your Structured Installment Sale

A structured installment sale annuity can provide sellers with guaranteed payments over a designated period. Before proceeding with a real estate transaction, it’s imperative to evaluate all options and find the best insurance company for your client.

Your client will be counting on the insurer to provide this income for years or decades to come. It’s important to find a company with a proven track record of making long-term annuity payouts through varying economic conditions. You should also make sure to review other indicators of an insurer’s reputation and credibility, such as its credit rating and Financial Quality statements.

An insurance company’s guarantee is only as good as their financial quality and strength. Don’t hesitate to ask for information about how the company is investing their assets to ensure that they can meet the long-term guarantees that your structured installment sale provide.

And finally, it’s always a good idea to ask an insurer about the ongoing support they offer following a structured installment sale. Do they have digital tools that allow you to easily access your account online? What about customer support lines?

| Metropolitan Tower Life Insurance Company is a leader in the insurance space and structured settlement market | ||

| As the insurer, Metropolitan Tower Life Insurance Company issues the annuity contract and distributes payments to the seller. | ||

|

||

|

||

|

||

|

||

| For more credit rating information, visit our corporate profile here. |

Pursuing a structured installment sale is an important decision that can impact your client’s tax liability and future financial security. Be thorough as you research insurance companies and evaluate all the pertinent information available to determine which one is best for your client.

For more information, please contact:

Paul Marshall - Sales Director

pmarshall1@metlife.com

Philippe Petit - Sales Director

ppetit@metlife.com